|

Here are five things I will do when negotiating a home purchase for you.

When is the right time to have a conversation with your favorite real estate pro about your home ownership dreams and goals? The sooner the better. As your realtor, I'm able to help you sort out your situation so you can make informed decisions about what to do and when to do it. No pressure, just help and support. Let's set up a time to talk.

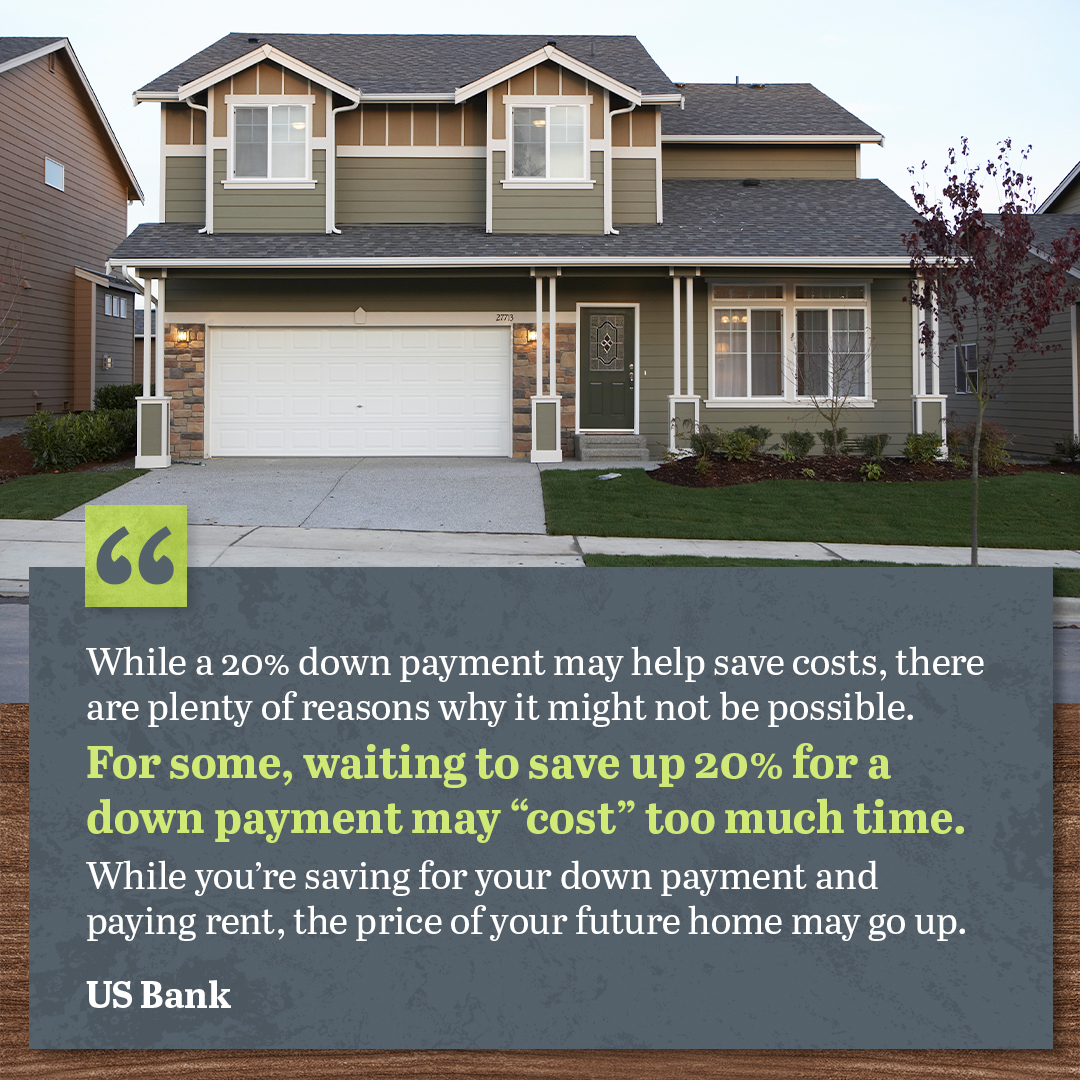

Worried about saving 20% for a down payment? You might not need to. Plus, time is money, and taking the time to save that much could cost you more in the long run. That’s because while you’re saving, rising rents and home prices are working against you, and you’re missing out on building home equity.

It's important to be prepared to buy BEFORE you see the house you want to buy! Let's get your financing, budget, and goals sorted out so you're ready to go when you see a house you love!

If you're choosing between renting or buying a home this year, consider that homeownership can be a significant wealth-building tool. Let’s connect so you can learn more about how buying a home can increase your net worth over time.

|

POST TOPICS

All

DAVID BURKUMWhen buying or selling a home, it's important to understand the market and gain helpful insights to help you achieve the best results.

Archives

April 2024

|